Real Estate Agents Are Feeling The Burn

In the economic maelstrom within which we find ourselves thrashing around this fall, there’s been plenty of talk about the potential housing crash ahead and the future layoffs that could fuel it, but I’ve seen only a few passing comments on the job losses and pay cuts we’re almost certain to sustain within the real estate industry itself.

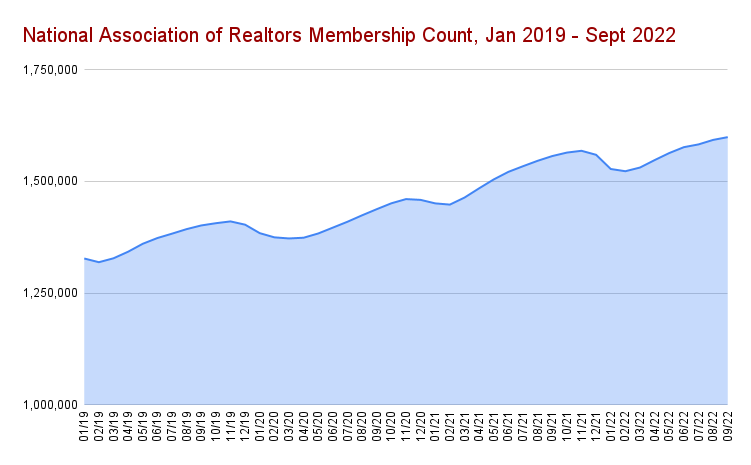

There are more than 3 million people holding active real estate licenses in the United States, according to the Association of Real Estate License Law Officials (ARELLO). The vast majority of these are unsalaried, receive no benefits, and earn a 100% commission-based income. Due to the extreme and immediate sensitivity of agent and broker earnings to market conditions, they might be among the first to have their wages severely impacted by the recession.

Even if home prices stay relatively stable in 2023 (a big if), depressed sales activity is likely to gouge away a sizable percentage of the earnings of those 3 million agents. Existing home sales in September were down 23.8% YoY, according to the National Association of Realtors. At this rate, an agent who makes $100k/year would see their annual income drop to something in the family of $76,000 if sales don’t go down any further and prices stay the same. With ample reason to believe that both of these metrics will decline in 2023, let’s just say the forecast is pretty grim.

I’m going to share my story at the risk of revealing the wet spots behind my ears, because I think it’s an illustrative one. In the summer of 2019, I got my real estate license and sold a few homes part time. I left my job when COVID hit and subsequently dove into real estate full time (and then some). Although I already had my license, I was effectively part of that record-breaking wave of agents who entered the industry in 2020 and 2021. In those two years put together, more than 156k new agents began their careers; that’s 60% more than in the two years prior.

While the real estate licensure exam is no joke, getting started as an agent is almost embarrassingly easy relative to other careers with a similar earnings potential. The mandatory pre-licensing course can be completed in 3 months for about $400 (less with a Groupon; I’m not kidding). There are longer, more rigorous, and more expensive routes to the same destination, but as every agent will tell you, 95% of what must be memorized in order to pass the test is useless once you begin your career. Real estate is truly an apprenticeship profession. For this reason, many agents-in-training opt for the quick n’ dirty path to licensure.

At least 20% of US workers decided to change careers during the pandemic. Real estate’s low barrier to entry, high earnings potential, and a record-busting housing boom were all potent motivators. According to Google Search Trends, the top job-related search in 2021 was “how to become a real estate agent”. That year, we all repeatedly heard the media quip about there being more agents in the USA than there were homes for sale. And while low inventory did mean that one’s work with a buyer was likely to be prolonged and arduous, for those who were willing to put in the hours, making money in real estate was like shooting fish in a barrel. Everyone and their brother was buying, and at least in my area, most serious shoppers were eventually ending up in new homes.

As a newly full time agent in spring of 2020, the fire under my ass was a profession to which I was not eager to return. I worked about 70 hours a week almost every week for two years. Hard work paired with a booming market allowed me to double my 5-year sales goal in my first year as a full time agent.

The truth is, similarly motivated new agents are unlikely to have the same results in 2023. It’s tough to get started in real estate. In order to be any good, you really need to treat learning the ropes like a full time job. It’s essentially an unpaid internship; you don’t make any money until you manage to convince someone that you know what you’re doing, and for a while, you don’t. In the meantime, you have to pay a laundry list of dues and fees in order to keep the machinery running. It is for this reason that 87% of agents put their licenses in escrow before their 5 year anniversary.

I predict that a record number of agents will hang up their Realtor® hats and find a different way to pay the bills in 2023. Many first-time buyers, the population most likely to work with newer agents, are getting priced out of the market and opting to rent. And older agents who were approaching retirement might decide that this is an opportune time. We’ve seen this before. In 2005-2006, 250k Americans got their real estate licenses (even more than 2020-2021). After the 2008 crash, 10% of agents left the industry.

What we’re expecting to see in 2023 is a “flight to quality”; fewer transactions will be consummated, and the buyers and sellers who remain in the market are likely to be anxious and in need of an expert to help them navigate it. The experienced and the highly scrappy alone will persevere. With an oversaturated pool of real estate professionals and a housing market farting its way into oblivion like a rapidly deflating balloon, there’s no other way.

I haven’t even brushed on the many real-estate-adjacent professions that are poised to share in the pain: lenders, inspectors, brokers, title companies, wholesalers, appraisers, real estate lawyers, developers, contractors, and more. My favorite Philly home inspector recently told me that he hasn’t had this little business in 16 years. We’re talking about a massive sector of the workforce; depressed transaction volume will affect all of them, regardless of what prices do. What makes agents particularly vulnerable to these housing market shifts is the fact that if we don’t close deals, we don’t get paid… not in six months, but today. There is no security net. Those of us who make it through the next few years will need a high pain tolerance, a high skill level, and a high savings account balance.

Kira Mason come to Prince William county, VA! Where the real estate market still thrives, unfortunately.

We moved here in JUNE 2021 and rented a home for $2850. One year later, (Aug 2022) our landlord panicked and put our house up for sale for $757k. We had no showings for a month, she dropped to $700k and we started getting showings. She gave up on October 1st and decided to wait until summer of 2023 to try again. Our rent went up to $3,500!

When our home was being sold, we got an experienced real estate broker in her 50's and started looking to buy in Aug,2022. There was nothing on the market under $600,000 to buy. Most homes were around $800k, up from $550k in 2019.

In October, we went to an open house for a 1950's stone farm house. We went because it was $501k. It was a house in bad need of extensive renovations. The tiny 70 yr old bathrooms were all original and very sad. The kitchen needed a complete overhaul. We left thinking they are going to have a hard time selling this crappy house. It sold that week, much to my chagrin. The higher interest rates have brought the sweet spot down from $800k to $650k in what I am seeing sell. But anything under $600k goes fast if it is not in need of major repairs. The inventory is starting to rise and there are definitely more choices now in late October than there were in August. But if I look at "Pending Sales" on the MLS Link that my realtor allows me to use, they are still selling in all price ranges, especially if it has 1-10 acres of land included. They just sold 3 pre-construction homes on Lake Front Lots for $1 million each. So the money is still flowing west of Washington DC. We are like a lot of buyers who have decided we will pay $3500 in rent and wait to see if the market continues to turn in our favor. In the meantime, we still go to Open Houses and watch what sales to get a good feel for the market. Our realtor told us that the market here never turned down in the 2008-2010 bear market. I thought that was usual realtor marketing blather, but now, I am starting to believer her. If mortgage rates just leveled off here, this market would be fine. Sure there are sellers, like 2 of my coworkers, who paid $550k in 2019 and have their homes listed for $775 now and they are not selling, but look how greedy they are. Those homes would sale at $650-$625k, no doubt in my mind. You have sellers splitting into different camps of "want to sale for last June prices" and "we have to sale and we are more reasonable about the current market conditions". My landlord I guess is in the 3rd camp of "I am pulling the house off the market and waiting for the FED to Pivot " camp. So there will be some extra inventory hiding in the bushes when mortgage rates do turn around. I wrote this because our whole life in Aug/Sept was a panic of we are losing our home and we are going to be out in the streets if we don't buy something. Thankfully, we could not find anything to buy before our landlord took our home back off the market. Now we are an opportunistic buyer. We hope the FED blows up the housing market just in time for us to purchase something.

I think you're spot on with your prediction, Kira. What I'm seeing is a palpable sense of desperation not only among real estate agents (among those who are in the know) but also real estate brokers, who most assuredly are working on their 2023 profit and loss statements and are seeing declining production numbers for the coming year. Heck, I've received 3 solicitations this week from brokers wanting me to "come to the other side". Additionally, you've also got mortgage lenders, who with their Instagram selfies and TikTok dance moves are promising low interest rates in 2023, so "just buy now and refinance next year". Horrible, horrible financial advice, when as we know rates will only go down when the Fed reverses course, stops the rate hikes, and goes back to quantitative easing. Another great article!